Wah, crucial moment!

I think is good to monitor and wait for market confirmation!

Yearly dividend is 17 cents. Yield is 4.73%. NAV 4.22.

Pls dyodd.

TA wise, bearish mode!

If 3.60 cannot hold the high chance she will go down to test 3.53/3.50. Breaking down of 3.50 plus high volume we may likely see her going down to test 3.28 than 3.00 and 2.94.

Pls dyodd.

Wilmar Intl - Results is out Net profit is down 52.7% to 550m, Total Revenue is down 10% to 32538m.

Declared same interim dividend of 6 cents.

Lower contribution from Food and Feed and I industrial products despite higher sales volume.

Free cash flow of 1.89b.

I think the results is not bad!

Let's see how she fares next week!

Please dyodd.

Looks like she has managed to bounce-off from the low of 3.59 and rises higher to close well at 3.81, looks rather interesting!

Short term wise I think she may rise up to test 3.90. If it cannot stay above 4.00 then high chance it may roll down again!

Let's monitor and see how it turns out!

Results is due on 11th August.

Pls dyodd.

Indeed, she has come down to cover the Gap at 3.59. Looks rather interesting!

I think high probability we may see a rebound!

At 3.59, yield is about 4.73%. I think yield is quite decent! To get 5% yield, we will need to wait for 3.40 to come back!

Please dyodd.

Wah, looks like she is falling down to test 3.75 level soon!

If 3.75 cannot hold, next , she might be going down to fill the Gap at 3.59.

Please dyodd.

Wilmar International Limited, founded in 1991 and headquartered in Singapore, is today Asia’s leading agribusiness group. Wilmar is ranked amongst the largest listed companies by market capitalisation on the Singapore Exchange.

At the core of Wilmar’s strategy is an integrated agribusiness model that encompasses the entire value chain of the agricultural commodity business, from cultivation and milling of palm oil and sugarcane, to processing, branding and distribution of a wide range of edible food products in consumer, medium and bulk packaging, animal feeds and industrial agri-products such as oleochemicals and biodiesel. It has over 500 manufacturing plants and an extensive distribution network covering China, India, Indonesia and some 50 other countries and regions. Through scale, integration and the logistical advantages of its business model, Wilmar is able to extract margins at every step of the value chain, thereby reaping operational synergies and cost efficiencies.

Supported by a multinational workforce of about 100,000 people, Wilmar embraces sustainability in its global operations, supply chain and communities.

An Expanding Global Footprint:

From its humble beginnings, Wilmar has today become a global leader in processing and merchandising of edible oils, oilseed crushing, sugar merchandising, milling and refining, production of oleochemicals, specialty fats, palm biodiesel, flour milling, rice milling and consumer pack oils:

- Largest edible oils refiner, specialty fats and oleochemicals manufacturer as well as leading oilseed crusher, producer of consumer pack oils, flour and rice and one of the largest flour and rice millers in China

- One of the largest oil palm plantation owners and the largest palm oil refiner and palm kernel and copra crusher, specialty fats, oleochemicals and biodiesel manufacturer in Indonesia and Malaysia

- Largest producer of branded consumer pack oils in Indonesia

- Largest branded consumer pack oils, specialty fats and oleochemicals producer and edible oils refiner as well as leading oilseed crusher, sugar miller, refiner and ethanol producer in India

- One of the largest investors in oil palm plantations, one of the largest edible oils refiners and producers of consumer pack oils, soaps and detergents as well as third largest sugar producer in Africa

- Largest raw sugar producer and refiner, a leading merchandiser of consumer brands in sugar and sweetener market and largest manufacturer of bread, spreads and sauces in Australia

- Leading refiner of tropical oils in Europe.

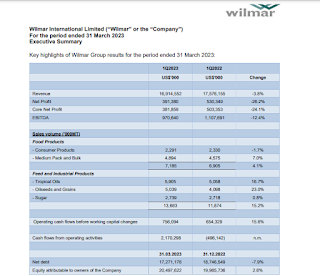

First quarter 2023 Financial No. update :

The Group reported net profit of US$391.4 million and core net profit of US$381.9 million for the quarter, with stronger sales volume recorded in both Food Products and Feed & Industrial Products segments. Excluding the gain on dilution of interest in Adani Wilmar Limited of US$175.6 million recognised in 1Q2022, the Group reported a growth in net profit of 10.3%, while core net profit grew by 16.5% during the quarter.

Despite the challenging operating conditions, the Group managed to deliver a satisfactory set of results for 1Q2023. Higher volume of sales was achieved across all businesses. Sugar milling and merchandising did well with higher sugar prices. Oilseed crushing did better due to higher volume and good coverage of raw materials. Food Products segment saw an overall increase in volume of sales, largely due to higher medium pack and bulk products sales, particularly in China. Plantation profit was reasonable even though palm oil prices came down significantly from the peak. Shipping performed well but palm oil refining margin was poor.

Cash Flow & Balance Sheet The stable performance for the quarter led the Group to generate higher operating cash flows before working capital changes of US$756.1 million. With the decline in commodity prices and seasonal reduction in overall inventory balance during the quarter, working capital requirements for the Group decreased accordingly, leading to lower net debt of US$17.27 billion as of 31 March 2023 (31 December 2022: US$18.75 billion). Consequently, net gearing ratio for the Group improved to 0.84x as of March 2023 (FY2022: 0.94x). This led to the Group generating strong cash inflow from operating activities of US$2.17 billion in 1Q2023. At the end of the reporting period, the Group had unutilised banking facilities amounting to US$26.32 billion.

Outlook Results for the quarter ended 31 March 2023 were satisfactory, despite the uncertain macro-economic outlook at the start of the year. With our diversified and integrated business strategies, we are cautiously optimistic that performance for the rest of the year will remain satisfactory.

The company paid out Final dividend of 11 cents + interim dividend of 6 cents, total 17 cents for FY 2022. The current share price is $3.97, yield is about 4.28% of which I think is quite a decent yield!

Chart wise, bearish mode!

She may likely continue to trend lower!

Short term wise, I think likely to go down to test 3.90.

Breaking down of 3.90 plus high volume that may likely see her falling down further towards 3.75 then 3.46 level.

Please dyodd.