I think something is brewing judging from the price movement long greenish candlestick! She is up 93 cents to 28.62, Superb!

I think this bullish momentum may push the price higher towards 29.00 than 30.17.

Please dyodd.

It looks like bargain hunters has come in to support. The price has managed to touch the high 0f 28.13 before settling down at 27.83 looks like Buying interest is back!

If it can overcome the resistance at 28.60 smoothly we may likely see her rising up to cover the Gap at about 29.00.

Results is near the corner and if it a gd sets of financial numbers plus a slight increase in dividend I think price may get lifted!

Please dyodd.

TA wise, she has continued to trend lower today down 16 cents to close at 27.24 , looks like Bear is in control!

I think she may go down to test 27.10 then 27.00.

If 27.00 cannot hold then next, we may see her testing 26.40 then 25.94.

Please dyodd.

Chart wise, bearish mode!

She has continued to trade lower and closed at 27.51, looks rather weak!

Short term wise, I think likely to test the pivot low of 27.32.

Breaking down of 27.32 plus high volume we may see her drifting down to test 27 then 26.50 with extension to 26.00.

First half results will be out on 27th July!

Please dyodd.

She is still stucked in a consolidation mode price patterns looks like mkt is giving us chance to monitor her direction!

Today she is down 14 cents to close at 27.82 , yield is about 4.82% seems quite interesting!

NAV 24.46.

Please dyodd.

Chart wise, bearish mode!

She is stucked in a consolidation mode!

Short term wise, if she is able to reclaim 28.60 and filled up the Gap at 28.88 that would likely reverse this downtrend!

Yearly dividend of 1.35. Yield is about 4.8+%.

Pls dyodd.

UOB is rated as one of the world's top banks, ranked 'Aa1' by Moody's Investors Service and 'AA-' by both S&P Global and Fitch Ratings. With a global network of 500 branches and offices across 19 countries in Asia Pacific, Europe and North America.

In Asia, we operate through our head office in Singapore and banking subsidiaries in China, Indonesia, Malaysia, Thailand and Vietnam, as well as branches and offices throughout the region.

The recent acquisition on 11 May 2023:

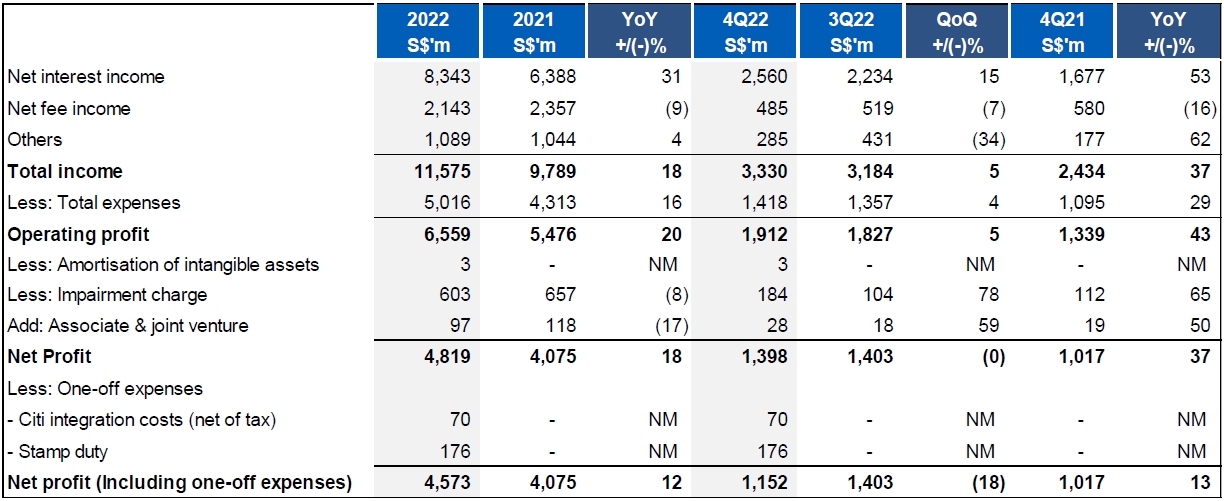

UOB’s acquisition of Citigroup’s consumer banking businesses in four key ASEAN markets has significantly boosted its retail banking business, and paved the way for its enlarged base of customers in the region to enjoy even more perks and privileges suited to their unique lifestyles and needs via partnerships with renowned domestic and global brands.

The completion of UOB’s acquisition of Citigroup’s consumer banking businesses in Malaysia, Thailand and Vietnam has already brought its regional retail customer count to over seven million as of 31 March 2023, with the latest completion of the Vietnam acquisition enabling the Bank to serve about 200,000 customers in the country. With the completion of the acquisition in Indonesia by end 2023, these four markets are expected to provide a S$1 billion boost to the Bank’s revenue on a full-year basis. The acquisition has also built stronger resilience in the business model with both geographical and revenue mix diversification. With Citigroup’s portfolio more geared towards cards business and unsecured lending, net credit card fees for the Bank almost doubled year-on-year in the first quarter of 2023, with Citigroup’s portfolio contributing a quarter of this, and total income from the Bank’s unsecured business is expected to almost double by end 2023. Separately, loans and deposits also grew almost 10 per cent and 15 per cent in the first quarter of 2023 compared with a year before.

p style="background-color: white; box-sizing: border-box; color: #333333; font-family: "Open Sans", Arial, Heiti, sans-serif; font-size: 15px; margin: 0px 0px 10px;">

For the first quarter of 2023, ASEAN-4 (i.e. Malaysia, Thailand, Indonesia and Vietnam) accounted for more than 35 per cent of the Bank’s Group Personal Financial Services income. UOB’s network of branches in Malaysia, Thailand and Vietnam has also expanded by 15 as of March 2023.

UOB

Beer Thai (1991) Public Company Limited

Beer Thai (1991) Public Company Limited